Dive Brief:

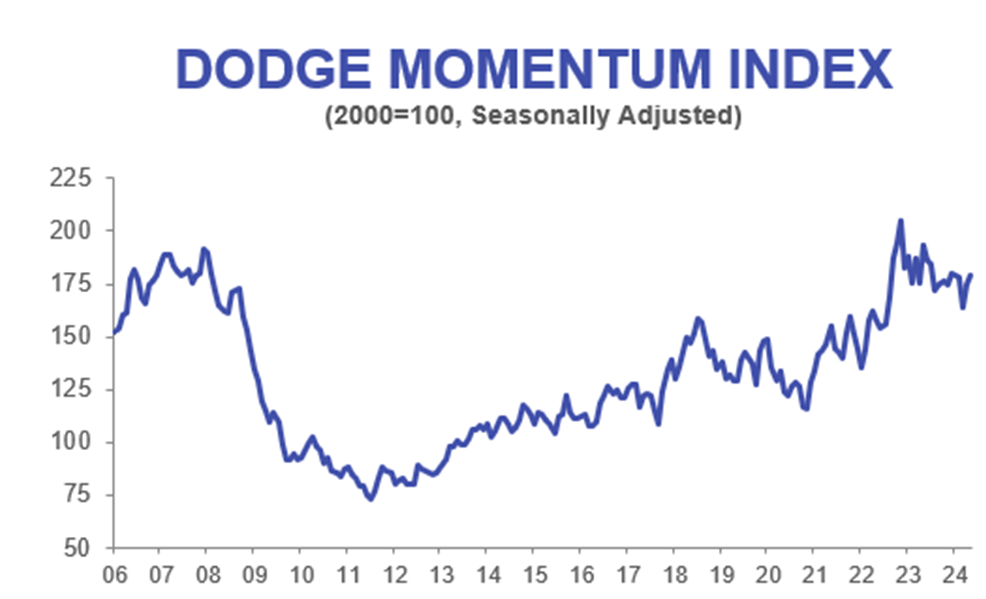

- The Dodge Momentum Index, a benchmark that measures nonresidential construction planning, increased 2.7% in May due to growth in sectors like offices and data centers, according to the Dodge Construction Network.

- Planning in the institutional sector — such as education, life sciences and healthcare — slowed by 3.4%, while commercial planning, which makes up office, industrial and data centers, jumped 5.5% over the month.

- “Owners and developers are gaining confidence in 2025 market conditions, alongside more stable and predictable interest rates — spurring stronger commercial activity over the month,” said Sarah Martin, associate director of forecasting at Dodge Construction Network. “Conversely, after last year’s growth, institutional planning is decelerating, as high material costs, labor shortages and elevated interest rates seep into planning decisions.”

Dive Insight:

A total of 19 U.S. projects valued at $100 million or more entered planning during May. The largest commercial sector projects included:

- The $500 million renovation of the former Mirage Hotel to a Hard Rock Hotel and Casino in Las Vegas.

- A $495 million Prime data center in Fort Worth, Texas.

- A $481 million Prime data center in Garland, Texas.

The largest institutional projects to enter planning included:

- The $377 million renovation of Neyland Stadium at the University of Tennessee.

- The $350 million Woodland Research and Technology Office in Woodland, California.

Martin noted the overall DMI is 40% higher than the pre-pandemic levels seen in May 2019. It also indicates a steady pipeline of construction projects that will be ready to break ground through mid-2025.

Data center planning continued to support growth on the commercial side of the index in May, alongside a steady acceleration in retail planning over the last six months as well. Marginal increases in project activity also helped prop up hotel and warehouse planning in May, according to Dodge.

On the other hand, healthcare and education planning activity slowed for the third consecutive month. That continues to constrain total institutional planning momentum, according to Dodge.

The DMI remained 7% lower than year-ago levels, following an abnormally strong May 2023. However, the commercial segment jumped 8% from May 2023, while the institutional segment dropped 32% over the same period.

The Architectural Billings Index, an indicator of construction work nine to 12 months out, continues to remain soft, according to the most recent data from the American Institute of Architects. It said that the value of newly signed design contracts dipped slightly in April, as clients stay hesitant to commit to new work

Architecture firms had been anticipating a springtime reduction in interest rates from the Federal Reserve. However, with that expected decrease now potentially postponed until late summer or fall, architects, and the contractors they work with, should brace for a continuation of slower months ahead, the AIA said.