Dive Brief:

- Commodity prices will come down before the end of 2022 but supply chain issues will persist for years and a recession is on the horizon in 2023, a leading construction economist predicted.

- In a James Bond-themed presentation titled "No Time to Buy," Associated Builders and Contractors Chief Economist Anirban Basu emphasized the historic price inflation dogging contractors, with input prices for construction rising 24.4% year over year through February.

- Planned interest rate hikes will likely temper those increases by year's end, he said, but will also lead to a short-lived economic contraction. "The Federal Reserve has engaged in eight interest rate tightening cycles since the early 1980s," Basu said. "Six have ended in recession."

Dive Insight:

Basu's current economic outlook portends a tougher bid environment for contractors going forward as they try to add new jobs to their pipelines in the face of even higher price escalations. In 2021, Basu challenged the Fed's outlook that rising inflation was a transitory event, a view that proved prescient.

But while Basu's presentation focused on the longer-term impacts of inflation, the supply chain, labor shortages and the war in Ukraine, it also outlined continued expansion for the immediate future.

"This will be a year of growth, but 2023 could be very different," Basu said during a webcast with ABC members March 30. He pointed to the prospect of "stagflation" on the horizon, the combination of a tepid economy amid unusually high price increases.

He predicted that when first-quarter GDP numbers come out this month, they'll show just 1% growth, but that inflation will continue to rise. "As long as you have supply chain issues, you still have price escalations," Basu said. "And I think 2023 could get that kind of stagflation."

Supply chain issues, which have hit construction harder than the broader economy and have pushed prices for critical materials such as steel mill products up by 74.4% in the last twelve months, will persist, according to Basu.

No magic wand

Due to much of the world still dealing with COVID-19, and many countries not having as plentiful access to vaccines as the U.S. to inoculate workers, he said there would still be a lag in the global production of materials.

"Even if COVID went away tomorrow and the Russia-Ukraine war ended, these supply chain troubles last into 2023 and in some cases 2024," he said. "It takes a long time to build capacity."

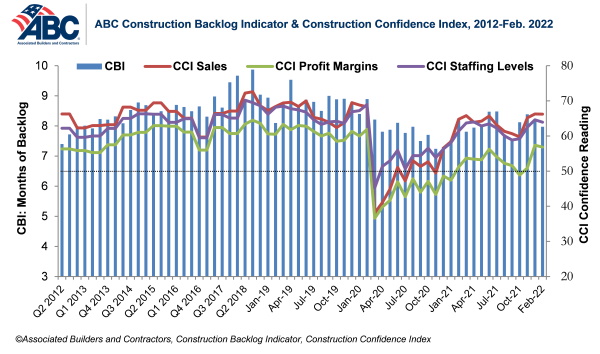

Despite these challenges, contractor optimism has largely stayed positive. But cracks are beginning to show in that outlook, as contractors' expectations for profit margin growth have begun to flatten, according to ABC's Construction Confidence Index.

The lack of supplies will continue to drive inflation to an even greater degree than current government projections, in Basu's view. While the Fed is forecasting 4.3% inflation in 2022, Basu pegged his outlook closer to 5%.

"Along with rising wages amidst the Great Resignation, this unbalanced economy translates into higher-than-average inflation in 2022," Basu said.

Given that outlook, he advised transportation officials to back weight their spending of dollars from the $1.2 trillion bipartisan infrastructure act until 2024 or 2025, when they will buy more for taxpayers.

"If you try to rush this, you're going to be delivering or receiving construction services at a time when prices are really high and capacity is really constrained," Basu said. "If I was a director of transportation in a certain state, I would spread out the construction work" over two to four years, he said.

By contrast, one bright spot has been the apartment sector. While most commercial contractors focus on nonresidential projects, there is crossover for some on multifamily developments.

"Apartment permitting is skyrocketing," Basu said. "Some of you are involved in that multifamily market, and so that should be one of the stronger markets for you going forward."

In spite of that momentum, Basu pointed to evidence that inflated pricing and persistent labor shortages are already causing owners to hit the brakes on proposed nonresidential projects.

He cited recent growth in the Architectural Billings Index, which tracks early stage design work and is hence used as a leading indicator for construction down the road. But that data hasn't aligned with actual nonresidential fixed investment in structures as tracked by the U.S. Bureau of Economic Analysis, which has mostly fallen during the pandemic.

The reason why, Basu postulated, is that investors who have mandates to put capital to work have pressured developers to at least start outlining projects. But once they get to the bid phase, inflationary cost overruns have forced them back to the sidelines.

"I would think that there would be even more construction taking place based on design work that's transpiring," Basu reasons. But project owners looking at their pro forma — or the projected return on their projects — are seeing a disconnect with actual bids. The thinking at that point from developers is, "'My pro forma is therefore busted, and I can't move forward with this project,'" Basu said.

Good news

The silver lining of the outlook came from commodity futures. Basu said projected economic weakness in China, paired with decreased commodities futures pricing due to anticipated interest rate hikes, likely mean some relief is in sight.

"For many of these other commodities, like steel, I think these prices are going to fall significantly later this year," Basu said.

In other words for construction, right now is no time to buy. At least not yet.

{kind=link}